Buying property in Mallorca remains one of the most popular investment and lifestyle strategies for international buyers in Europe. The island consistently ranks among the most desirable regions in Spain for purchasing a second home, investment property, or a permanent residence.

According to Spanish banks and real estate agencies, approximately 55–65% of property transactions in Mallorca involve mortgage financing (mortgage Mallorca), particularly among international buyers.

The reason is simple: mortgages in Spain remain relatively accessible, and Spanish banks actively work with international clients. Today mortgage Mallorca can be obtained by both residents of Spain and non-residents, including citizens of Germany, the United Kingdom, Switzerland, Scandinavian countries, and many others. This makes buying property on the island far more flexible from a financial perspective.

At the same time, obtaining mortgage Spain foreigners has its own specific requirements. Banks carefully evaluate a borrower’s income, asset structure, tax residency, and the origin of funds. It is also important to understand the differences between mortgage rate types, down payment requirements, early repayment conditions, and additional costs involved in obtaining financing.

In this comprehensive guide we explain how to get mortgage Mallorca in 2026, which banks offer the best conditions, how much capital you need to buy property, and what steps must be completed from submitting a mortgage application to signing the mortgage agreement with a Spanish notary.

If you are just starting to explore the island’s property market, we also recommend reading our market analysis.

Read our detailed overview of the Mallorca real estate market: Mallorca Real Estate Market 2026: Prices, Forecast & Investment Guide

In this guide, specialists from Aventin Real Estate Mallorca explain the entire mortgage process in detail — from bank requirements to practical examples of monthly mortgage payments. This will help you understand how to safely and efficiently buy property for sale Mallorca using mortgage financing while minimizing risks and additional costs.

Who Can Get a Mortgage in Mallorca: Borrower Requirements

Both Spanish residents and foreign citizens living outside Spain can obtain mortgage Mallorca. Spanish banks actively work with international property buyers, which makes Spain mortgage for non residents a common practice, particularly in high-demand markets such as Mallorca.

Most mortgages on the island are issued to buyers from European Union countries including Germany, France, the Netherlands, Belgium, Sweden, as well as the United Kingdom and Switzerland. However, Spanish banks may also consider applications from borrowers in other countries if they can demonstrate stable income and transparent financial documentation.

To obtain mortgage Spain foreigners, borrowers must meet several key requirements established by Spanish banks.

Main Mortgage Requirements for Borrowers

Requirement | Description |

|---|---|

Verified income | Banks require official proof of income such as salary statements, dividends, business income, or investment income |

Financial stability | Stable employment or business activity for at least 1–2 years is preferred |

Credit history | Positive credit history in the borrower’s country of residence |

Borrower age | Usually between 21 and 70–75 years by the end of the mortgage term |

Down payment | Availability of personal funds for the initial deposit |

Documentation | Passport, NIE tax number, bank statements, and income verification |

For non-residents, banks typically finance 60–70% of the property value, while Spanish residents may qualify for higher financing ratios.

It is important to understand that each bank evaluates applications individually. In addition to income, banks analyze debt obligations, the type of property being purchased, and the overall financial profile of the borrower.

For this reason many international buyers planning to buy property Mallorca first obtain a mortgage pre-approval, allowing them to clearly understand their available purchase budget.

Can You Get a Mortgage in Germany to Buy Property in Mallorca?

Many European buyers — particularly from Germany — ask whether it is possible to obtain financing for property in Mallorca from a bank in their home country rather than applying for a Spanish mortgage.

In theory this is possible, but in practice it is far less common than obtaining mortgage Mallorca directly from a Spanish bank.

The main reason is that banks usually prefer to issue mortgage loans secured by property located in the same country where the bank operates. If the property is located in Spain, a German bank must arrange a property valuation, legal verification, and collateral registration in another jurisdiction. This significantly complicates the process and increases administrative costs.

Nevertheless, some large European banks and private financial institutions may offer financing for clients purchasing property for sale Mallorca. In such cases several financing structures may be used.

Possible Financing Options in Germany

Option | Description |

|---|---|

Loan secured by property in Germany | The buyer uses an existing property in Germany as collateral |

Large consumer loan | Sometimes used for smaller financing amounts |

International mortgage programs | Certain banks offer financing for overseas property purchases to high-net-worth clients |

Despite these options, most international buyers prefer obtaining Spain property mortgage directly from Spanish banks. This is due to a more transparent process, better financing conditions, and the fact that the mortgage collateral is registered in the same country where the property is located.

In addition, Spanish banks actively work with international buyers and offer dedicated programs for mortgage Spain foreigners, specifically designed for non-resident clients.

As a result, the financing process for those planning to buy property Mallorca is typically faster and more straightforward when working with Spanish banks.

Are There Differences Between Mortgage Programs in Mainland Spain and Mallorca?

One of the most common questions from property buyers is whether mortgage Mallorca conditions differ from mortgage programs offered by banks in mainland Spain.

In most cases, there are no major differences between mortgage programs, since Spain’s banking system is regulated by unified national legislation and common lending rules.

The largest Spanish banks operate throughout the country and offer the same core mortgage products both on the mainland and on the islands. This means that the conditions of a Spain property mortgage — including interest rates, maximum loan terms, borrower requirements, and the application process — are generally the same regardless of the region.

Typical Mortgage Conditions in Spain

Parameter | Typical Conditions |

|---|---|

Maximum mortgage term | up to 25–30 years |

Financing for Spanish residents | up to 80% of property value |

Financing for non-residents | usually 60–70% of property value |

Interest rate types | fixed, variable, or mixed |

Maximum debt-to-income ratio | around 30–35% of borrower income |

However, in practice there may be minor differences related not to the region itself but to the specific real estate market.

For example, on Mallorca many banks pay closer attention to property valuations in premium areas such as Palma de Mallorca, Son Vida, or Puerto Andratx. This is mainly because Mallorca real estate is one of the most expensive and sought-after property markets in Spain.

It is also important to note that in regions with very high demand for property, banks may analyze transactions more carefully. Nevertheless, the overall process of obtaining mortgage Spain foreigners and the core lending conditions remain the same across the entire country.

This makes buying property and arranging financing for those planning to buy property Mallorca a transparent and relatively straightforward process whether the property is located on the mainland or on the island.

How Much Mortgage Can You Get in Mallorca?

The amount of mortgage financing (mortgage Mallorca) depends on several key factors: the borrower’s status (Spanish resident or non-resident), income level, property value, and the borrower’s financial history.

Spanish banks use a fairly transparent model for calculating mortgage financing.

In most cases, the bank finances a percentage of the official property valuation, not necessarily the purchase price. If the property valuation is lower than the purchase price, the mortgage will be calculated based on the lower valuation amount.

What Percentage of the Property Value Can Be Financed?

Borrower Type | Maximum Financing |

|---|---|

Spanish residents | up to 80% of property value |

Non-residents | usually 60–70% |

Premium clients | sometimes up to 70–75% |

This means that buyers planning to buy property Mallorca must have their own funds available for the down payment.

Required Down Payment

Category | Required Own Funds |

|---|---|

Non-resident buyers | 30–40% of property value |

Spanish residents | 20–30% |

Additional purchase costs | around 10–12% of property price |

For example, when purchasing property for sale Mallorca valued at 1,000,000 €, a non-resident buyer typically needs around 400,000–450,000 € in personal funds (including the down payment and transaction costs).

Maximum Debt-to-Income Ratio

Spanish banks follow a financial stability rule: the monthly mortgage payment should generally not exceed 30–35% of the borrower’s net income.

Indicator | Value |

|---|---|

Recommended debt ratio | up to 30% of income |

Maximum possible ratio | 35–40% in certain cases |

When reviewing an application for Spain mortgage for non residents, banks analyze not only the borrower’s income but also existing loans, family expenses, and overall financial assets.

Types of Mortgage Rates in Spain

Spanish banks offer several mortgage programs for property buyers. The main difference between them is the structure of the interest rate.

When applying for mortgage Mallorca, borrowers can choose between a fixed rate, variable rate, or mixed mortgage.

The choice of mortgage type directly affects monthly payments, financial risk, and the total cost of the loan over time.

Main Mortgage Types in Spain

Mortgage Type | Key Characteristics | Suitable For |

|---|---|---|

Fixed rate | Interest rate remains the same for the entire loan term | Buyers who want stable payments |

Variable rate | Rate linked to Euribor index and can change | Buyers expecting interest rates to fall |

Mixed rate | Fixed rate for initial years, then variable | Balance between stability and flexibility |

Fixed Rate Mortgage

With a fixed rate mortgage, the interest rate remains unchanged throughout the entire loan term — typically 20–30 years.

This allows borrowers to know the exact monthly payment in advance.

This option is particularly popular among buyers applying for mortgage Spain foreigners, as it provides financial predictability.

Parameter | Value |

|---|---|

Typical interest rate | 2.8% – 3.7% |

Mortgage term | up to 30 years |

Payment changes | none |

Variable Rate Mortgage

A variable mortgage rate depends on the Euribor index, which is updated several times per year. Banks add a fixed margin to this index.

Example:

Euribor + 1.2%

If Euribor increases, the mortgage payment increases as well. If Euribor decreases, the payment becomes lower.

Parameter | Value |

|---|---|

Starting rate | 2.2% – 3.0% |

Rate review | every 6–12 months |

Risk factor | changing monthly payments |

Mixed Mortgage

The mixed mortgage model is becoming increasingly popular in Spain.

In this structure, the mortgage has a fixed interest rate during the first years (usually 5–10 years) and then automatically converts into a variable rate mortgage.

Period | Interest Type |

|---|---|

first 5–10 years | fixed rate |

remaining term | Euribor + bank margin |

This option is often chosen by buyers considering Mallorca property investment, as it provides stability in the early years while allowing potentially lower rates in the future.

In the next section we will examine current mortgage Mallorca rates in 2026 and the offers from the largest Spanish banks.

Current Mortgage Rates in Mallorca in 2026

Interest rates for mortgage Mallorca are determined by Spain’s overall banking policy and depend primarily on the Euribor index, which is the main benchmark for mortgage lending across Europe.

At the beginning of 2026, Euribor is approximately around 2.2%, which directly influences the cost of mortgage loans throughout Spain.

As a result, most Spanish banks currently offer mortgage rates ranging from approximately 2.5% to 3.7% annually, depending on the type of mortgage, borrower profile, and additional banking products (insurance, salary transfer, etc.).

Average Mortgage Rates in Spain (2026)

Rate Type | Average Rate Range (2026) |

|---|---|

Variable rate | 2.5% – 2.9% |

Fixed rate | 2.8% – 3.7% |

Mixed rate | 2.7% – 3.4% |

The most competitive mortgage offers are usually available to clients with higher income levels and when purchasing property priced above 300,000 €, which is typical within the Mallorca real estate market.

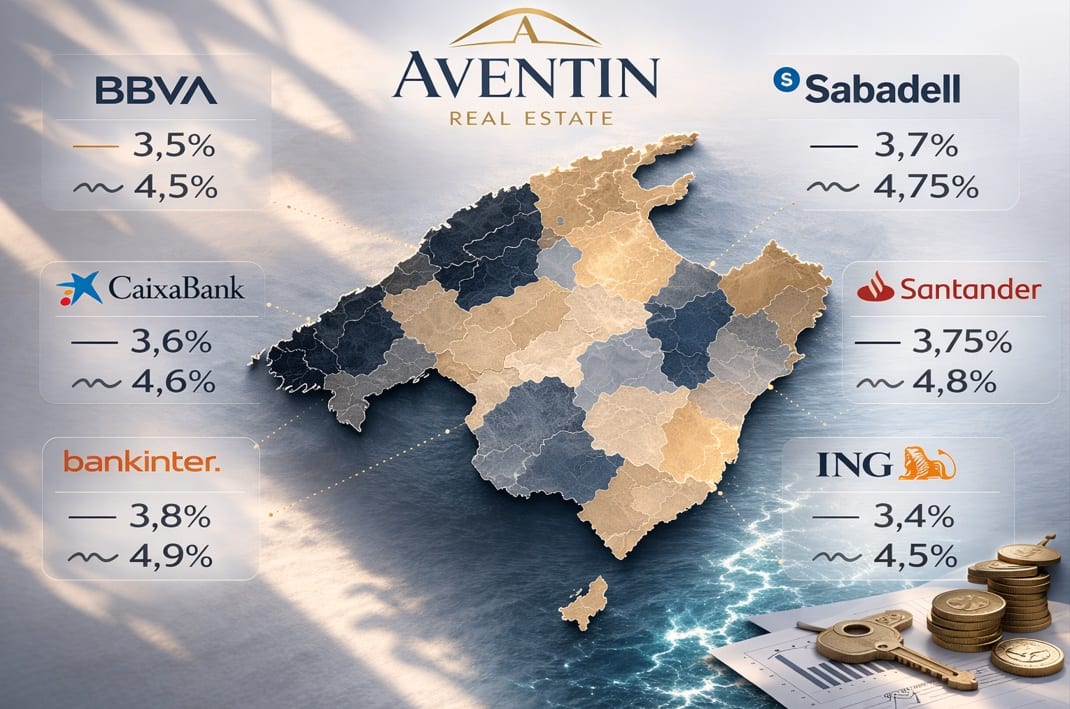

Major Banks Offering Mortgage in Mallorca

Almost all major Spanish banks provide mortgages for purchasing property for sale Mallorca. The following institutions are among the most popular banks for international buyers.

Bank | Rate Type | Approximate Rate | Maximum Term | Key Features |

|---|---|---|---|---|

Banco Sabadell | fixed / variable | from ~3.45% | up to 25–30 years | popular among international buyers |

BBVA | fixed | around ~3.6% | up to 25–30 years | actively finances non-residents |

CaixaBank | fixed / mixed | from ~3.5% | up to 30 years | one of the largest Spanish banks |

Santander | fixed / variable | ~2.55–3.55% | up to 30 years | competitive programs for new clients |

Bankinter | fixed / variable | ~3.0–3.6% | up to 30 years | often offers strong conditions for residents |

ING | variable | Euribor + ~0.8% | up to 25–30 years | one of the lowest margin spreads |

What Determines Mortgage Interest Rates

Banks determine mortgage rates individually for each borrower. Several factors influence the cost of Spain mortgage for non residents.

Factor | Impact on Mortgage Rate |

|---|---|

Down payment size | the larger the deposit, the lower the rate |

Income and financial stability | higher income reduces bank risk |

Property value | premium properties are easier to finance |

Additional bank products | insurance and salary transfers may reduce the rate |

Residency status | residents often receive slightly lower rates |

On average, borrowers with a strong financial profile can expect mortgage rates of around 3–3.3% annually when purchasing property in Mallorca.

This makes mortgage Spain foreigners one of the most accessible ways to finance real estate purchases in Europe.

In the next section we will examine all the costs associated with obtaining a mortgage in Mallorca, including bank fees, property valuation, insurance, and mortgage broker services.

Costs of Getting a Mortgage in Mallorca

When applying for mortgage Mallorca, buyers must consider not only the down payment but also additional expenses associated with obtaining mortgage financing.

In Spain, legislation in recent years has redistributed some mortgage costs, meaning that many bank-related fees are now covered by the bank itself. However, borrowers still incur several mandatory expenses.

On average, the total additional costs involved in obtaining a Spain property mortgage amount to approximately 10–12% of the property price, including purchase taxes and transaction-related costs.

If we focus specifically on mortgage-related expenses, several key categories apply.

Main Mortgage Expenses

Expense Type | Description | Approximate Cost |

|---|---|---|

Property valuation (Tasación) | Independent valuation required by the bank to determine market value | 300 – 700 € |

Notary fees | Signing of the mortgage contract | paid by the bank (by law) |

Mortgage registration | Registration of the mortgage in the property registry | paid by the bank |

Mortgage opening fee | Some banks charge an arrangement fee | 0 – 1% of the loan |

Property insurance | Mandatory insurance for the mortgaged property | 200 – 600 € per year |

Life insurance (optional) | Sometimes required to reduce bank risk | depends on borrower age |

Additional Costs When Buying Property

It is important to remember that when purchasing property for sale Mallorca, there are additional expenses not directly related to the mortgage but required for completing the transaction.

Expense | Approximate Amount |

|---|---|

Property Transfer Tax (ITP) | 8 – 13% depending on property value |

Notary and registry fees | 1 – 2% |

Legal services | 1 – 1.5% |

Property due diligence | depends on transaction complexity |

Mortgage Broker Fees

Many international buyers prefer arranging mortgage Spain foreigners through a mortgage broker.

A broker helps choose the most suitable bank, prepare documentation, and negotiate better mortgage conditions.

Service | Cost |

|---|---|

Mortgage program selection | often free |

Full mortgage assistance | around 0.5 – 1% of loan amount |

In some cases the broker’s commission is paid by the bank, meaning the service may be free for the client.

Mortgage Insurance

Spanish banks usually require at least one mandatory insurance policy — property insurance.

Banks may also offer additional products such as:

life insurance

mortgage payment protection insurance

borrower income insurance

Subscribing to these financial products can sometimes reduce the interest rate on mortgage Mallorca by 0.2–0.5%.

When planning to buy property Mallorca using mortgage financing, it is essential to account for all associated costs in advance. This allows buyers to accurately calculate their transaction budget and avoid unexpected financial obligations.

Step-by-Step Mortgage Process in Mallorca

Obtaining mortgage Mallorca is a structured process that consists of several consecutive stages. On average, arranging a mortgage takes between 4 and 8 weeks, depending on the bank, the complexity of the transaction, and how complete the borrower’s documentation is.

Below we explain the entire process — from the initial financial assessment to signing the mortgage agreement with a Spanish notary.

Main Steps of the Mortgage Process

Stage | What Happens | Timeframe |

|---|---|---|

Initial consultation | analysis of budget, income, and possible loan amount | 1–3 days |

Document preparation | collection of borrower financial documents | 3–7 days |

Pre-approval | the bank evaluates borrower solvency | 1–2 weeks |

Property valuation | an independent appraiser determines market value | 3–5 days |

Final approval | the bank confirms mortgage conditions | 3–7 days |

Notary signing | mortgage agreement signing and registration | 1 day |

1. Initial Budget Assessment

The first step is evaluating the buyer’s financial capacity. A bank or mortgage broker analyzes income, existing loans, and available savings.

This helps determine how much financing is possible under Spain mortgage for non residents and what property price range the buyer can consider.

At this stage many buyers begin searching for property for sale Mallorca, already having a preliminary understanding of their budget.

Villas for sale Mallorca

Apartments for sale Mallorca

Luxury property Mallorca

2. Document Preparation

To apply for mortgage Spain foreigners, a borrower must submit a set of financial documents. Typically banks require:

passport

NIE tax identification number

proof of income

tax declarations

bank statements

employment contract or company documents

For entrepreneurs and business owners, the list of required documents may be longer.

3. Mortgage Pre-Approval

After submitting documents, the bank performs a financial analysis of the borrower.

At this stage the bank determines:

maximum loan amount

mortgage rate type

estimated interest rate

Obtaining pre-approval significantly simplifies the property purchase process because the seller understands that the buyer already has financing secured.

4. Property Valuation

The next step is the official property valuation (tasación).

The bank appoints an independent appraiser who determines the market value of the property.

The valuation usually costs 300–700 €, and its result directly affects the amount of mortgage Mallorca the bank is willing to provide.

5. Final Mortgage Approval

After the property valuation, the bank makes its final decision and issues the official mortgage offer called FEIN (Ficha Europea de Información Normalizada).

This document specifies:

interest rate

loan term

monthly payment

additional mortgage conditions

Under Spanish law, the borrower must receive this document at least 10 days before signing the purchase transaction.

6. Mortgage Signing with a Notary

The final stage is signing the mortgage agreement simultaneously with the property purchase.

The transaction takes place at a notary office, after which the mortgage is registered in the Spanish Property Registry.

From that moment, the buyer officially becomes the property owner, and the bank receives the property as collateral.

If you are planning to buy property Mallorca using mortgage financing, specialists at Aventin Real Estate Mallorca can help organize the entire process — from selecting the right property to working with banks and completing the transaction.

Early Mortgage Repayment in Mallorca

In Spain, borrowers have the right to repay mortgage Mallorca early, either partially or in full. This allows homeowners to reduce the loan term or decrease their monthly mortgage payments.

Early repayment is regulated by Spanish banking legislation, and most mortgage programs include this option.

Types of Early Repayment

Repayment Type | What Happens |

|---|---|

Partial repayment | borrower pays an additional amount and reduces the monthly payment or loan term |

Full repayment | the mortgage is completely closed |

Banks may charge a small early repayment fee depending on the type of mortgage rate.

Early Repayment Fees

Mortgage Type | Early Repayment Fee |

|---|---|

Fixed rate mortgage | up to 2% during the first years |

Variable rate mortgage | usually up to 0.25–0.5% |

In practice, many property owners in Mallorca use early repayment to optimize their financial commitments.

Example from Real Practice

A buyer from Germany purchased a villa worth 1.2 million € and obtained mortgage Spain foreigners of 700,000 €.

Several years later, the property value increased and the buyer’s income grew. He made an additional payment of 150,000 €, reducing the loan term by 6 years and significantly lowering the total interest paid.

Another common scenario involves using funds from the sale of another asset or business to partially repay a mortgage after purchasing property for sale Mallorca.

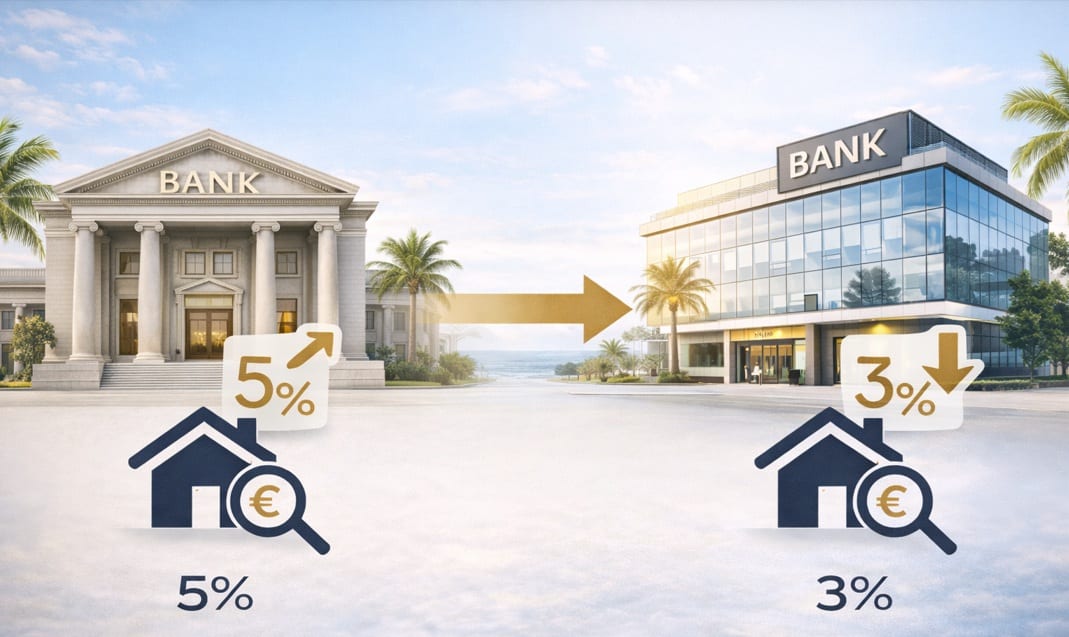

Mortgage Refinancing and Transferring a Loan to Another Bank

Over time, mortgage conditions may become less favorable. In such cases borrowers can use mortgage refinancing (mortgage Mallorca) or transfer their mortgage to another bank.

In Spain this process is called subrogación de hipoteca.

Refinancing allows borrowers to change mortgage conditions — for example, reduce the interest rate, change the loan term, or switch from a variable rate to a fixed rate mortgage.

Main Reasons for Mortgage Refinancing

Reason | What Changes |

|---|---|

Lower interest rate | reduces monthly payments |

Change of rate type | switch from variable to fixed |

Loan term adjustment | shorten or extend the mortgage |

Debt consolidation | combine multiple loans |

Transferring a Mortgage to Another Bank

If another bank offers better Spain property mortgage conditions, borrowers can transfer their mortgage.

The new bank pays off the remaining loan with the current bank and issues a new mortgage contract.

Step | Description |

|---|---|

Request conditions | new bank reviews the current mortgage |

Property valuation | new valuation is conducted |

Bank offer | new mortgage terms are prepared |

Signing the new mortgage | the mortgage transfer is completed |

In recent years, banks have been actively competing for clients, allowing many borrowers to reduce their mortgage rate by 0.5–1% through refinancing.

For example, if a property owner obtained mortgage Mallorca several years ago at 3.8%, while current market rates are around 3%, transferring the mortgage to another bank could significantly reduce total interest costs.

Refinancing is a popular tool among property owners who previously buy property Mallorca and now want to adjust their mortgage conditions to the current economic environment.

Selling Property in Mallorca With an Existing Mortgage

Situations where a property owner wants to sell real estate that still has an active mortgage Mallorca are quite common. In Spain this is a completely normal practice, and having an outstanding mortgage does not prevent the sale of a property. The key is to properly organize the transaction process and coordinate with the bank.

When selling property with an active mortgage, several scenarios are possible. The most common option is repaying the remaining mortgage balance at the moment of signing the transaction with the notary.

In this case, part of the funds paid by the buyer is transferred directly to the bank to repay the outstanding mortgage debt.

How a Property Sale With an Existing Mortgage Works

Stage | What Happens |

|---|---|

Request mortgage statement from the bank | the seller receives an official document showing the remaining mortgage balance |

Signing the purchase agreement | the buyer transfers funds for the transaction |

Mortgage repayment | part of the payment goes directly to the bank |

Removal of mortgage charge | the mortgage is removed from the property registry |

If the property price is higher than the remaining mortgage balance, the seller receives the difference between the sale price and the outstanding loan.

Transfer of Mortgage to the Buyer

In some cases, the buyer may take over the seller’s existing mortgage. This process is called mortgage subrogation (subrogación).

In this scenario, the buyer continues paying the existing loan under the same or modified conditions, provided the bank approves the buyer’s financial profile.

Real Examples from Practice

Case 1 — Selling a Villa With an Existing Mortgage

A property owner in southwest Mallorca purchased a villa for 950,000 € using a Spain property mortgage. After five years the property value increased to 1.25 million €, while the remaining mortgage balance was 420,000 €.

When the property was sold, the buyer transferred the purchase funds, from which the bank received the amount necessary to close the mortgage, and the seller received the remaining proceeds.

Case 2 — Transferring the Mortgage to the New Owner

A buyer purchased an apartment from the property for sale Mallorca market and agreed to take over the seller’s existing mortgage with an attractive 2.1% fixed interest rate obtained several years earlier.

The bank reviewed the buyer’s financial situation and approved the mortgage transfer.

Even if the mortgage has not yet been fully repaid, the owner can easily sell property in Mallorca. Proper transaction management allows the mortgage to be closed safely and the sale to be completed without complications.

Important Things to Consider When Getting a Mortgage in Mallorca

Before applying for mortgage Mallorca, it is important to consider several factors that directly influence mortgage conditions, approval timelines, and the overall financial strategy of purchasing property.

Over the past few years, the mortgage market in Europe has changed significantly due to global economic events.

Can a Mortgage Be Arranged Remotely?

Today most Spanish banks allow remote mortgage applications.

Buyers can begin the process of obtaining mortgage Spain foreigners from their home country by submitting documents, receiving preliminary approval, and negotiating mortgage conditions with the bank.

However, the final step — signing the mortgage agreement with a Spanish notary — usually requires personal presence in Spain. In some cases a notarial power of attorney can be used if the buyer cannot travel to Mallorca.

How Mortgage Rates Have Changed in Recent Years

The cost of Spain property mortgage has been significantly influenced by global economic events in recent years.

COVID-19 (2020–2021) — mortgage rates reached historic lows

Energy crisis and inflation (2022–2023) — rates increased sharply

Economic stabilization (2024–2026) — the market gradually adjusted

Despite rising rates after the pandemic, demand to buy property Mallorca remains strong.

Mallorca is considered one of the most stable real estate markets in Europe, which is why banks continue actively financing property buyers.

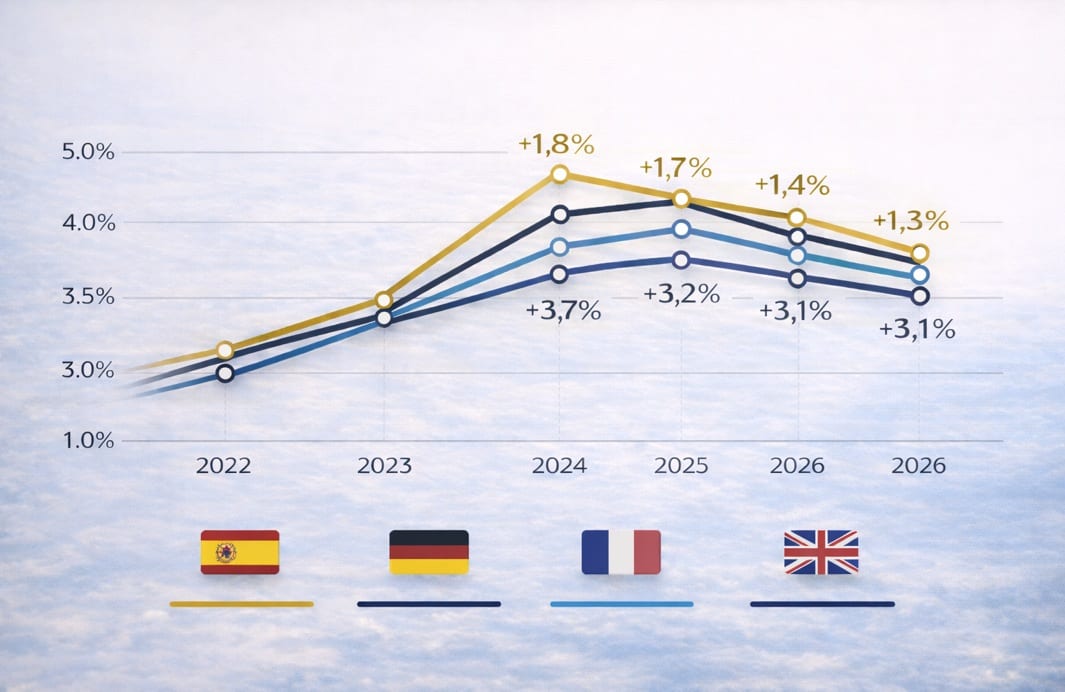

Mortgage Rate Comparison in Europe (2022–2026)

Country | 2022 | 2023 | 2024 | 2025 | 2026 | Change |

|---|---|---|---|---|---|---|

Spain | ~1.6% | ~3.4% | ~3.2% | ~3.1% | ~3.0% | +1.4% |

Germany | ~1.5% | ~3.7% | ~3.5% | ~3.3% | ~3.2% | +1.7% |

France | ~1.7% | ~3.5% | ~3.3% | ~3.2% | ~3.1% | +1.4% |

United Kingdom | ~2.0% | ~4.5% | ~4.2% | ~4.0% | ~3.8% | +1.8% |

As shown in the table, mortgage rates increased across Europe. Nevertheless, mortgage Mallorca rates remain competitive compared with other countries.

Are More Buyers Using Mortgages Today?

After the pandemic, the structure of the property market changed. In 2020–2021, many buyers purchased property using their own capital.

However, in recent years the share of transactions involving mortgages has increased again.

Today approximately 50–60% of property buyers in Mallorca use Spain mortgage for non residents or local mortgage programs.

This is because mortgage financing remains an effective financial tool for purchasing property and making long-term investments.

Changes in mortgage rates across European countries (2022–2026)

If you are planning to purchase property for sale Mallorca and considering mortgage financing, it is important to understand current market trends and plan the structure of the transaction in advance.

Specialists at Aventin Real Estate Mallorca can help you choose the most effective property purchase strategy and secure the best mortgage conditions.

Mortgage Calculation Example in Mallorca

To better understand how mortgage Mallorca works, let’s look at several practical mortgage calculation examples.

In most cases banks finance 60–70% of property value for non-residents and up to 80% for Spanish residents, while the mortgage term can reach 25–30 years.

Example 1 — Buying an Apartment in Mallorca

Parameter | Value |

|---|---|

Property price | 500,000 € |

Down payment (30%) | 150,000 € |

Mortgage amount | 350,000 € |

Interest rate | 3.2% |

Mortgage term | 25 years |

Monthly payment | ~1,690 € |

In this case the buyer uses Spain mortgage for non residents to purchase property for sale Mallorca and finances 70% of the property value.

Example 2 — Buying a Villa in Mallorca

Parameter | Value |

|---|---|

Property price | 1,200,000 € |

Down payment (35%) | 420,000 € |

Mortgage amount | 780,000 € |

Interest rate | 3.1% |

Mortgage term | 25 years |

Monthly payment | ~3,750 € |

Such calculations help buyers understand their transaction budget and evaluate whether monthly payments will be comfortable when planning to buy property Mallorca.

Mortgage Calculator — Estimate Your Monthly Mortgage in Mallorca

This calculator allows users to independently estimate mortgage payments, interest rates, and loan terms.

Frequently Asked Questions About Mortgages in Mallorca

Can I get a mortgage in Mallorca if I am not a Spanish resident?

Yes. Most banks offer mortgage Spain foreigners, allowing international buyers to finance 60–70% of the property value.

What is the minimum down payment required?

Non-resident buyers typically need 30–40% of the property value, plus additional funds for purchase costs (approximately 10–12%).

How long does it take to obtain a mortgage?

The process of obtaining mortgage Mallorca usually takes 4–8 weeks, including document verification, property valuation, and bank approval.

Can I repay my mortgage early?

Yes. Spanish banks allow both partial and full early repayment of mortgage loans. A small fee may apply depending on the mortgage rate type.

Can property purchased with a mortgage be rented out?

Yes, unless restricted by the mortgage agreement. Many investors buy property as Mallorca property investment specifically for rental income.

Can the mortgage process be completed remotely?

Most steps can be completed remotely. However, the final mortgage agreement usually needs to be signed with a notary in Spain.

Buying Property in Mallorca With a Mortgage

If you are planning to purchase property for sale Mallorca and are considering mortgage financing, specialists at Aventin Real Estate Mallorca will help guide you through the entire process — from selecting the right property to securing mortgage financing and completing the transaction.

More than 40% of Aventin Real Estate clients purchase property using mortgage financing, which means our team has extensive experience working with Spanish banks and international buyers.

We can help you:

choose the best property option

obtain mortgage pre-approval

select the bank with the best conditions

organize legal support for the transaction

Read our detailed articles as well:

Possible Break in US–Spain Economic Relations: What It Means for the Mallorca Real Estate Market

The “New York Effect”: Why Mallorca Is the New Luxury Hub for Global Investors

Mallorca Real Estate Market 2026: Prices, Forecast & Investment Guide

Property for Sale in Mallorca – Explore by Type and Location

To explore more property opportunities in Mallorca, browse our main categories below.

Whether you are looking to buy property in Mallorca, find villas for sale, explore apartments in Mallorca or discover new developments and investment properties, you will find carefully selected listings across the island’s most desirable areas such as Palma, Santa Ponsa, Cala Vinyes and Southwest Mallorca.

Start exploring Mallorca properties and find your perfect home today.

General Listings | Property Types | The Most Popular Locations | ||

|---|---|---|---|---|

Author: Aventin Real Estate Experts